New York LLC Law 2026 Formation Compliance and the Transparency Act

Introduction

New York LLC law moves fast. Really fast. If you advise clients or run your own firm, keeping up with these changes in 2026 matters more than ever.

This year brings some of the biggest shifts in recent memory. The New York LLC Transparency Act took effect on January 1, 2026. That means LLCs formed or registered in New York must now file beneficial ownership information reports within 30 days of formation. The rules are new, and the penalties for missing them can be steep.

New York LLC law covers a lot of ground. Formation rules, governance requirements, yearly compliance tasks, and dissolution procedures each come with their own deadlines and paperwork. Understanding the statutory law behind LLCs helps you avoid costly mistakes and serve your clients better. That is exactly why this guide exists.

We will walk you through the essential steps of forming an LLC in New York. You will learn about naming rules, how to file Articles of Organization with the New York Department of State, and what fees to expect. We will cover the governance rules that keep an LLC in good standing. And we will break down the compliance obligations you cannot afford to ignore in 2026.

Technology is changing how legal professionals handle all of this. Modern tools can streamline entity management, track deadlines, and reduce manual work. The role of a lawyer in 2026 looks different than it did just a few years ago, and staying current with both the law and the tools that support it gives you a real advantage.

Whether you are a seasoned business attorney or a solo practitioner diving into entity formation, this guide will save you time and worry.

Want to stay ahead of legal tech trends that affect how you practice law? The Deep View Newsletter delivers clear daily AI updates straight to your inbox.

Let us dive in.

Formation of a New York LLC: Step-by-Step in 2026

So you are ready to form an LLC for a client. The process in 2026 has clear steps.

But a few details can cause problems if you rush. Understanding the statutory law behind formation helps you guide your clients safely.

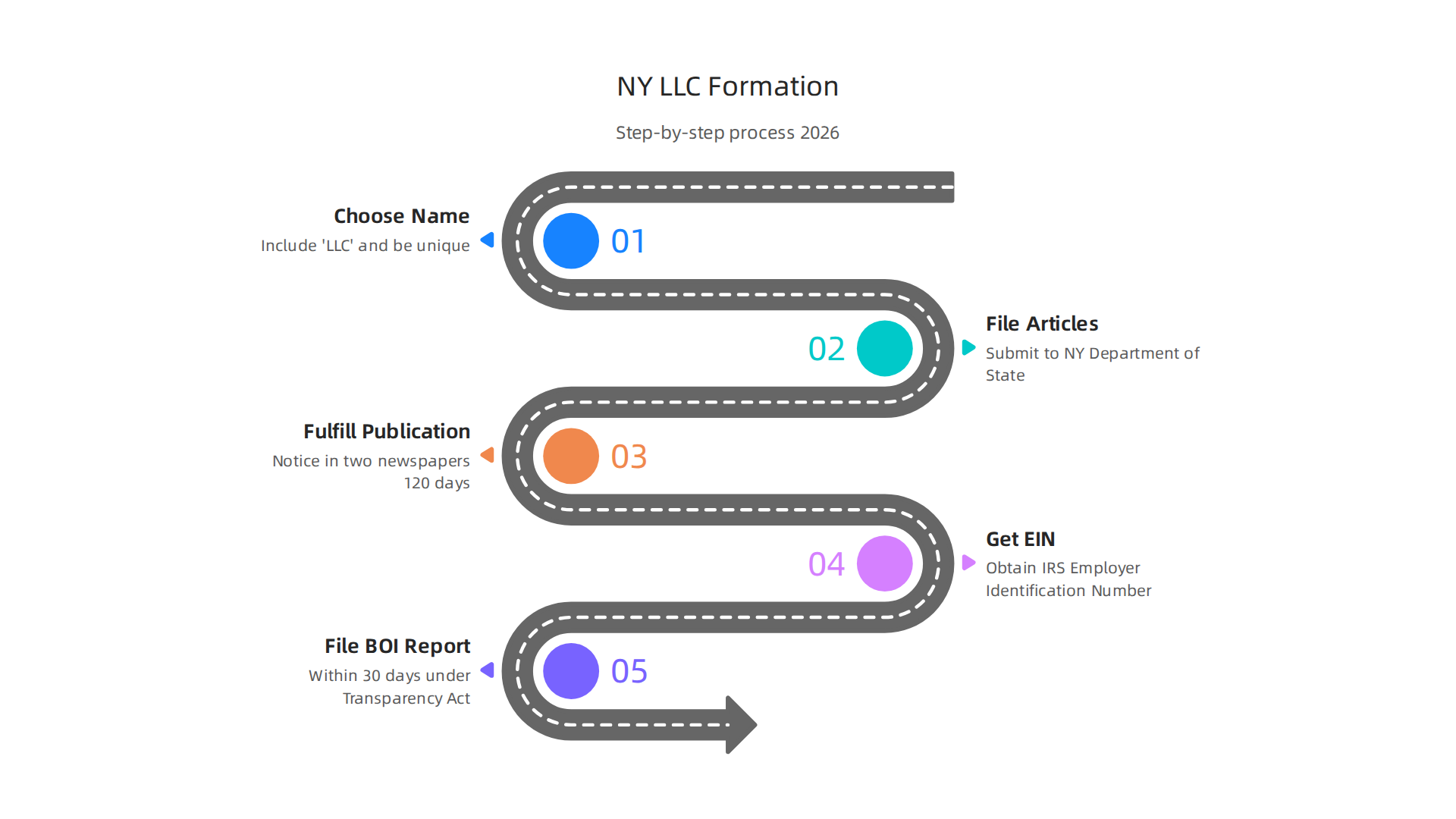

Step 1: Choose a Name That Follows the Rules

The name must include "LLC" or "Limited Liability Company." It also needs to be unique in New York. You can check name availability on the New York Department of State website before you file. If you want to hold a name while you finish the other steps, you can reserve it for 60 days.

Step 2: File the Articles of Organization

This is the main filing. You send the Articles of Organization to the New York Department of State. According to Tailor Brands, the total fee is $205. That includes the $200 filing fee plus a $5 fee for a non-certified copy. Filing online is faster than by mail.

Step 3: Fulfill the Publication Requirement

New York has a rule most states do not. Within 120 days of filing, you must publish a notice in two newspapers. One in the county where the LLC is located, and one in the city. This is a common pitfall. Forgetting this step can lead to losing the LLC’s authority to do business.

Step 4: Get an EIN

You need an Employer Identification Number from the IRS. It is free and you can get it online in minutes. You need an EIN to open a bank account and file taxes for the LLC.

Step 5: File the Beneficial Ownership Information Report

Here is the biggest 2026 change. Under the New York LLC Transparency Act, any LLC formed on or after January 1, 2026 must file a BOI report within 30 days. This report must include information on the beneficial owners. Missing this deadline carries penalties. This is now a key part of New York LLC law. You can learn more from the Morgan Lewis article on the NY LLC Transparency Act.

Using Technology to Manage the Process

Managing all these steps for multiple clients is easier with the right tools. New York LLC law requires attention to detail. Technology can track deadlines, store documents, and send reminders. This frees you up to focus on the legal advice your clients need. For more on how tech is changing the attorney role, see how technology reshapes the attorney role.

Stay Informed on Legal Tech

The law keeps changing, and so does the tech that helps you manage it. Get clear daily AI updates that matter to legal professionals. The Deep View Newsletter delivers them straight to your inbox.

Drafting an Operating Agreement: Key Clauses and Best Practices

You finished the formation steps. Your client is now a real LLC. But the work is not done yet. Every New York LLC needs a written operating agreement. According to Section 417 of the New York LLC Law, members must adopt one before, at the time of, or within 90 days after filing the Articles of Organization. The New York Department of State says the same thing. This is a legal requirement, not just a good idea.

Why does this matter so much? Without your own agreement, the default rules in New York LLC law take over. Those defaults might not fit your client’s situation at all. For example, the law might split profits equally among all members, even if one member put in more money. That can cause real problems later. A written operating agreement lets you tailor the rules to your client’s specific needs.

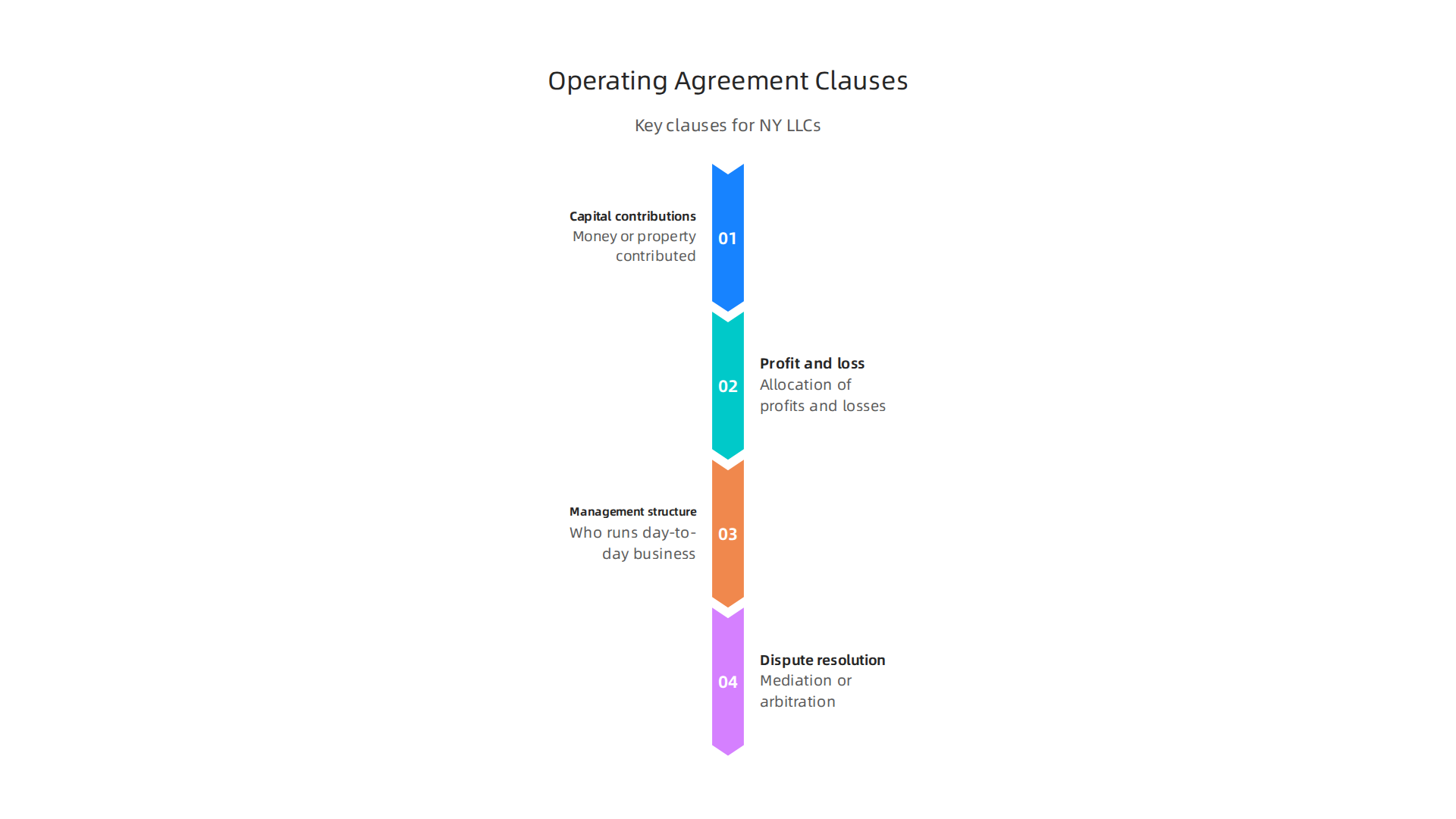

Here are the key clauses you need to cover:

- Capital contributions. How much money or property each member puts in. What happens if someone fails to contribute on time.

- Profit and loss allocations. How you split the money and losses. You can use a percentage based on ownership or a different formula.

- Management structure. Who runs the day to day business. Manager managed or member managed. The Wolters Kluwer guide explains the options clearly.

- Dispute resolution. What happens when members disagree. Many agreements use mediation or arbitration to avoid court.

Drafting these clauses from scratch is time consuming. That is why many lawyers use templates. The free template from LLC University gives you a solid starting point. You still need to customize it for your client. But templates save hours of work.

Legal technology can help even more. Tools like Iris Law use AI to review contract language and spot issues. This makes drafting faster and more accurate. If you want to see how tech changes contract work, read our article on why you need more than a lawyer for business contracts. It shows how tools and expertise work together.

The bottom line: never let a client skip the operating agreement. It protects them if things go wrong. And it keeps you out of trouble too.

Want to stay updated on AI tools that make legal work easier? The Deep View Newsletter delivers clear daily updates right to your inbox. Subscribe here to stay ahead.

Membership and Ownership Structures in NY LLCs

Now you have drafted an operating agreement. But let’s zoom in on one of the most important parts. The operating agreement decides who owns the company and what happens when ownership changes.

Flexibility is your biggest advantage.

One of the best things about New York LLC law is how flexible it is. You can create different membership classes. One member might get profits but no voting rights. Another member might get paid first before everyone else. This is called a special allocation. It lets you customize ownership to fit your client’s exact needs.

What happens when people join or leave?

Life changes. People want to leave. New people want to join. Your operating agreement must have clear rules for admitting new members, transferring interests, and withdrawal.

Here is a real problem. A member wants to sell their stake. If your agreement does not stop it, they could sell to a complete stranger. Now you are stuck working with someone you never wanted in the business.

Under basic statutory law, a member can usually transfer their rights. But you might not want that. A strong operating agreement fixes this. It gives the other members the "right of first refusal." This lets the company control who becomes an owner.

How the agreement protects everyone.

Think about withdrawal. A member wants to leave. How much are their shares worth? If it is not in the agreement, you are guessing. That causes fights. The operating agreement should set a clear valuation method.

The consequences of skipping these rules are serious. The Farrell Fritz law firm explains the unintended consequences of not having a written agreement. One small disagreement can put the whole business at risk.

On a related note, if you are a legal professional handling formations, your own tools need to keep up. Modern practice demands modern technology. Read our guide on how to choose the best employment lawyers NYC in 2026 to see how technology is reshaping legal work.

Staying updated on these tools is easier than you think. The Deep View Newsletter delivers clear daily updates on AI and legal innovation right to your inbox. Subscribe here to stay ahead.

Compliance Requirements for New York LLCs: Annual Reports and Taxes

You have your operating agreement set. Good work. But forming the LLC is just the beginning. New York has ongoing rules you must follow. Miss them, and your LLC could get dissolved.

Here is what you need to know about compliance under new york llc law in 2026.

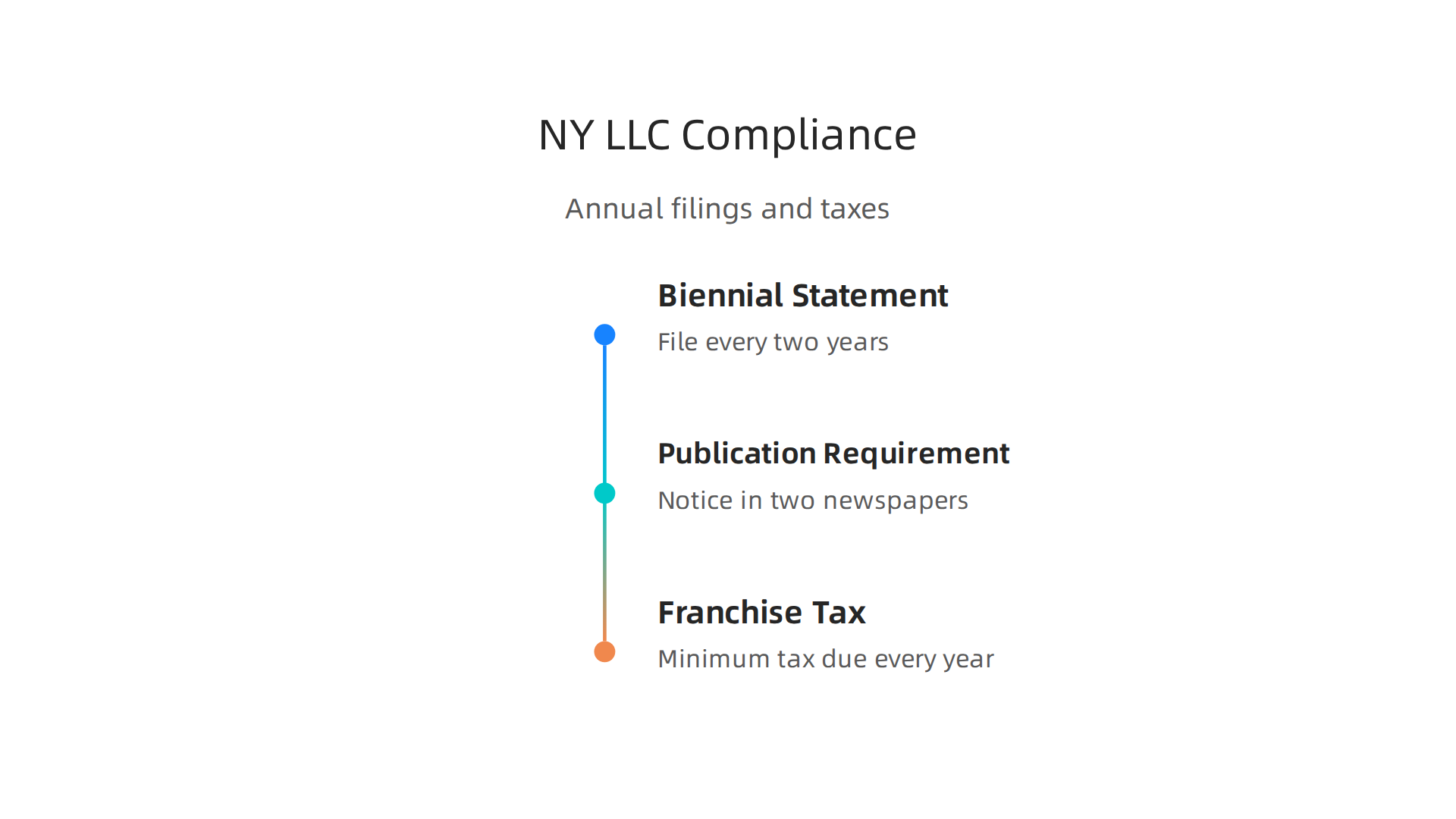

The Biennial Statement (Not an Annual Report)

Here is a common point of confusion. Many states require an annual report. New York does not. Instead, New York requires a Biennial Statement every two years. You file it with the Department of State using the e-Statement Filing System. The fee is only $9. But you have to file it during the exact calendar month your original articles of organization were filed. Miss this window and you face late fees and possible dissolution.

According to Nolo’s guide on NY LLC requirements, the biennial statement keeps your LLC in good standing. The LLC Annual Report Requirements by State comparison shows New York is unique in calling this a biennial statement rather than an annual report. Other states like Delaware skip the report entirely but charge higher franchise taxes.

The Publication Requirement

If you just formed a new LLC, you have another step. New York requires you to publish a notice in two newspapers for six consecutive weeks. One newspaper must be in the county where your LLC’s office is located. The other in the county where your principal business is located. You then file a Certificate of Publication with the Department of State. This is not optional. Ignoring it can hold up your ability to sue or defend your business in court.

Franchise Tax

Every NY LLC must also pay a minimum franchise tax. Under statutory law, the tax applies even if your LLC did not make money that year. The tax is due every year, not every two years like the biennial statement.

Consequences of Missing These Deadlines

The state does not send reminders. If you miss a filing or payment, penalties add up. Continued failure can lead to administrative dissolution. Once dissolved, you lose personal liability protection and must go through a formal reinstatement process. The state’s voluntary dissolution instructions show how serious New York treats these requirements.

How Legal Tech Tools Help You Stay Compliant

Filing dates are easy to forget. Especially when you manage multiple clients or your own growing firm. This is where modern legal tech tools make a real difference. Many platforms now offer automated compliance tracking. They send reminders for biennial statement due dates, franchise tax payments, and publication deadlines. Some even handle the filing process for you.

If you are building your practice around modern new york llc law, your tech stack matters. Staying updated on the best compliance tools and legal tech trends is easier when you have trusted sources. The Deep View Newsletter delivers clear daily updates on AI and legal innovation straight to your inbox. Subscribe here to stay ahead of changes that affect how you manage LLC compliance.

Liability Protection and Piercing the Corporate Veil

The main reason you form an LLC is to protect your personal assets. Under new york llc law, the LLC acts as a shield between you and the business debts. If the LLC gets sued or goes broke, creditors usually can’t touch your house, car, or savings. That is the promise of limited liability.

But this shield is not unbreakable. Courts can ignore it and hold you personally responsible. This is called piercing the corporate veil. As the Ohio State University Farm Office explains, piercing happens when a court decides the separation between you and your business no longer exists.

New York courts take this seriously. They look for specific red flags. According to muchmorelaw.com, the doctrine lets courts impose personal liability when owners misuse the LLC. The most common mistakes are simple but dangerous.

What gets you in trouble?

The biggest one is mixing your personal money with business money. Woods Law Group warns that moving funds back and forth between personal and business accounts is a major warning sign. Another big issue is not putting enough money into the LLC from the start. Lerner & Weiss calls this undercapitalization. If the LLC barely has enough cash to operate and then can’t pay a big bill, a court may say you set it up to fail.

Failing to keep proper records is another problem. First EP Business lists not following formalities like holding meetings or keeping minutes as common causes of piercing. And if you use the LLC to commit fraud, courts will tear the veil apart. Summit Law Group says fraud is the most common reason for piercing.

How to keep your shield strong

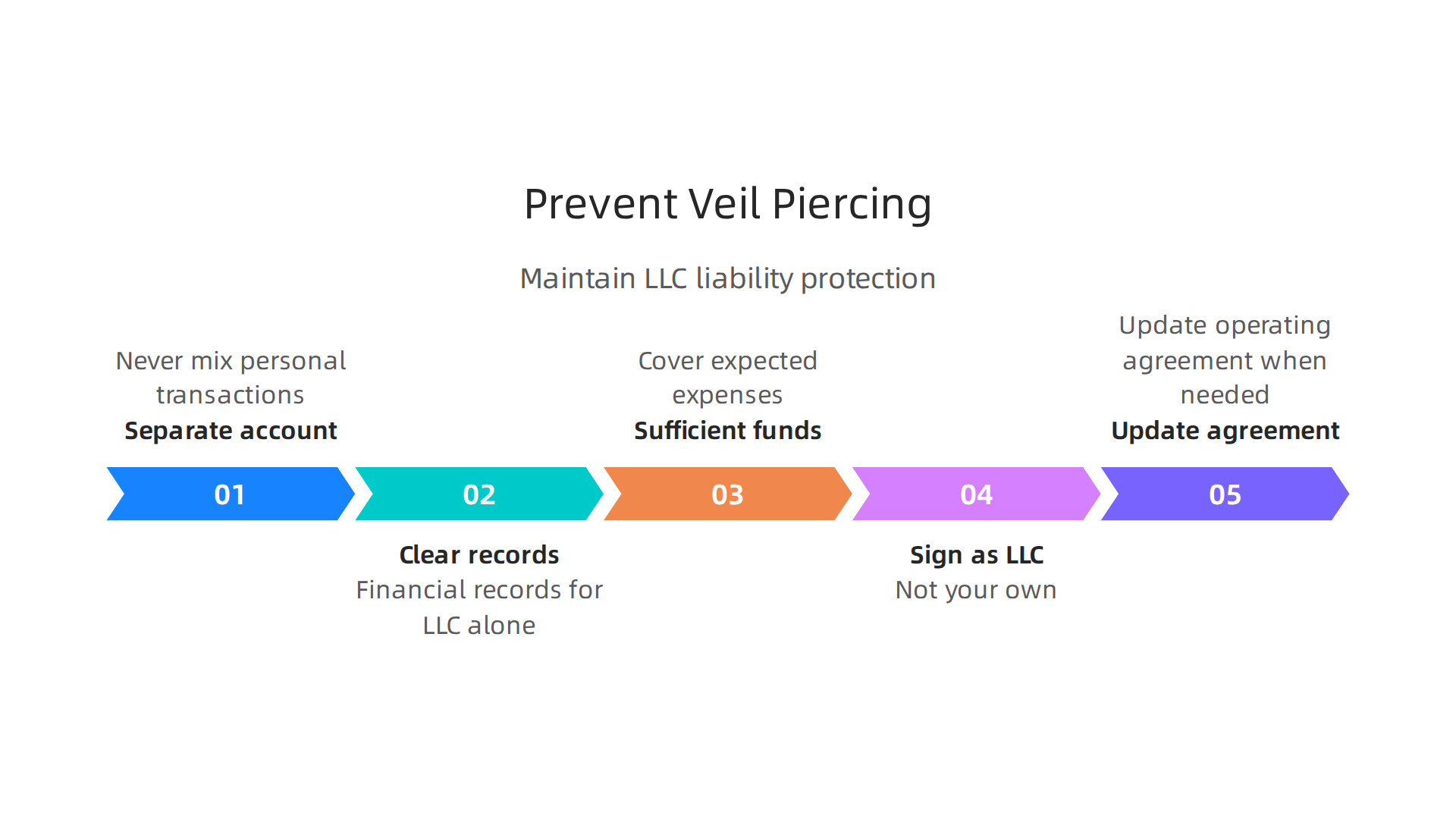

Protecting yourself is not hard. It just takes discipline. Here are the practical steps you need to follow under statutory law in New York:

- Open a separate business bank account and never mix personal transactions.

- Keep clear financial records for the LLC alone.

- Make sure the LLC has enough money to cover expected expenses.

- Sign contracts and agreements in the LLC’s name, not your own.

- Maintain your operating agreement and update it when needed.

One more thing: having a solid operating agreement and proper contracts helps prove the LLC is a real business. This article on why you need more than a lawyer for business contracts shows how good agreements protect you in many ways.

The bottom line

Piercing the corporate veil is rare, but it happens. If you treat your LLC like a real separate entity, your personal assets stay safe. Skip the formalities, and you put everything at risk. Staying organized and informed is your best defense.

Want to keep up with the latest tools and trends for managing LLC compliance and protecting your practice? The Deep View Newsletter delivers clear daily updates on AI and legal innovation. Subscribe here to stay ahead of changes that affect how you manage your business.

Dissolution and Winding Up of a New York LLC

Eventually, every LLC reaches the end of the road. Maybe you want to close the business.

Maybe the state forces it. Either way, dissolving your New York LLC the right way matters under new york llc law.

Here is the thing. If you just walk away and stop filing paperwork, the LLC still exists in the state’s eyes. That can cause problems later. You could still owe fees or face penalties.

Two ways an LLC ends

Voluntary dissolution happens when the members vote to close the business. You decide it is time to move on. Administrative dissolution is different. The state shuts you down for things like not filing your biennial statement or not paying taxes.

The steps you cannot skip

First, the members need to vote. Check your operating agreement to see what vote count you need. Then you file Articles of Dissolution with the Department of State.

But here is where many people slip up. You must settle all debts first. Statutory law in New York requires you to notify creditors and pay what you owe. The New York Tax Department also needs to clear you. You have to get written consent from the Tax Department showing you have no outstanding tax liability.

After that, you distribute any remaining assets to members. Finally, you close the business bank account and cancel any permits.

The big mistake to avoid

The most common pitfall is not filing the dissolution papers at all. You think just stopping operations is enough. It is not. The LLC stays active on state records. You keep owing the biennial statement fee. Fees pile up. Some people even get sued years later because they never formally ended the LLC.

Proper dissolution also means keeping good records of everything you did. That includes the vote, the creditor notifications, and the asset distribution. Having these records proves you followed public law 63-43 correctly and protects you from future claims.

Closing an LLC is not complicated. But it takes a few deliberate steps. Follow them carefully and you walk away clean. Skip them and the LLC becomes a headache that follows you.

Want to stay on top of compliance requirements that affect your business? The Deep View Newsletter delivers clear daily updates on legal changes and business trends. Subscribe here so you never miss important deadlines.

How Legal Tech Can Simplify New York LLC Management

Running an LLC in New York comes with a lot of paperwork. You have to file formation documents, keep up with biennial statements, track deadlines, and manage your operating agreement. Missing a single step can lead to fees or even losing your good standing.

That is where legal technology steps in. In 2026, there are tools that handle the boring stuff so you can focus on your business.

Here is how legal tech makes new york llc law easier to follow.

Automate formation and compliance

Setting up an LLC used to mean filling out forms by hand and hoping you got it right. Now platforms like Harbor Compliance guide you through every step. They check your name, file your Articles of Organization, and even appoint a registered agent. Once your LLC is active, software tools track your filing deadlines so you never miss a biennial statement.

The New York LLC Transparency Act went into effect on January 1, 2026. Non-U.S. LLCs now have to report beneficial ownership information. Staying on top of this new requirement is easier with platforms like NYLTA.com, which monitor your obligations and alert you when something changes. You can also find detailed compliance guidance from the Ron Cook Law Firm to avoid penalties.

AI-powered contract analysis

Your operating agreement is the backbone of your LLC. It defines member roles, voting rights, and profit splits. But reviewing these documents yourself can lead to mistakes. AI tools now analyze contracts in seconds. They highlight risky clauses, compare language against statutory law, and suggest improvements.

For example, IRIS Law uses artificial intelligence to review operating agreements and other legal documents. It catches things a human might miss, like vague dispute resolution terms or missing indemnification language. This saves you hours and reduces the chance of future conflict.

Real results you can measure

Legal tech is not just a nice to have. It delivers real time and cost savings. According to the Complete IT Compliance Checklist for NYC Law Firms, firms that adopt automation tools report cutting compliance work by up to 40 percent. That means fewer billable hours spent on routine tasks and more time for growing your business.

Small businesses also benefit. A solo practitioner in South Texas using legal tech cut their formation time from three days to one afternoon. Whether you are in New York City or somewhere else, the same tools work for you.

Where to go next

Legal tech is changing fast. New rules like the NY LLC Transparency Act and federal reporting requirements under public law 63-43 mean you need to stay informed. The best way is to subscribe to a daily update that breaks it all down.

Want clear, quick news on AI and legal compliance? Subscribe to The Deep View Newsletter so you never miss an important change.

Common Mistakes in New York LLC Formation and Operation

Even with great legal tech tools, people still trip up on a few key rules. Here are the most common errors that can mess up your new york llc law compliance.

Overlooking the publication requirement

New York is special. After you file your Articles of Organization, you must publish a notice in two newspapers for six weeks. Then you file proof with the Department of State. Skip this step? Your LLC can lose its authority to do business. The Wolters Kluwer guide to New York LLC formation covers this requirement in detail.

Mixing personal and business money

This is the fastest way to lose your liability shield. Courts can pierce the corporate veil if you treat your LLC bank account like your personal wallet. Common signs are paying personal bills from the business account or transferring money back and forth without reason. As the Woods Law firm explains, moving funds between personal and business accounts is a red flag. Keep everything separate. Use a dedicated business account and record every transaction.

Missing filing deadlines

New York requires biennial statements and, starting in 2026, annual beneficial ownership reports under the NY LLC Transparency Act. Late filings mean late fees. If you ignore them long enough, the state can dissolve your LLC administratively. Check the New York Department of State official page for current deadlines.

Legal tech can help you avoid all three mistakes. Automated reminders, document templates, and AI contract checks keep you on track. For a deeper look at how contracts can cause trouble, read our article on why you need more than a lawyer for business contracts.

Want to stay on top of every new rule and tech update? Subscribe to The Deep View Newsletter for daily AI and compliance news.

Summary

This guide explains New York LLC law in 2026 and walks you through formation, governance, compliance, liability protection, dissolution, and modern tools that make management easier. You will learn the exact steps to form an LLC—choosing a name, filing Articles of Organization, satisfying New York’s publication rule, and obtaining an EIN—as well as the new NY LLC Transparency Act requirement to file beneficial ownership information within 30 days. The article shows why a written operating agreement is mandatory and highlights key clauses to prevent disputes and control ownership transfers. It also covers recurring obligations like the biennial statement, franchise tax, and publication deadlines, and explains how poor recordkeeping or commingling funds can lead to veil piercing. Practical prevention tips and a rundown of legal tech—AI contract review, compliance trackers, and automation—help lawyers and business owners stay compliant and reduce risk. Read this to avoid common mistakes and streamline LLC workflows with the right processes and tools.